One has to be careful when analysts start using new and non-standard metrics for measuring market gains. So when a new metric of locations “passed or addressed” starts to be heard, one has to remain cautious about using any such figures in comparison to the traditional ways of measuring “homes or locations passed.”

Such non-standard terms have in the past been used when markets are changing fast, but also where financial meaning and sustainability are unclear. One good example was the concept of "voice grade equivalents" (VGEs) used in the turn of the century competitive telecom industry.

That concept was used in an effort to show account growth when bandwidth, rather than voice circuits, began to become the important revenue driver. The problem was that a

voice" circuit and a "bandwidth" service had quite different revenue implications. One no longer hears the term "VGE" used.

So it is useful to recall such precedents when using terms such as "locations addressed."

The term "location passed" has a specific meaning: a location has the ability to buy products from a service provider because the network already is built. That is important because it places a limit on the number of potential customers. A service provider, in other words, can fulfill a new service request at a location because the network actually exists to serve that location.

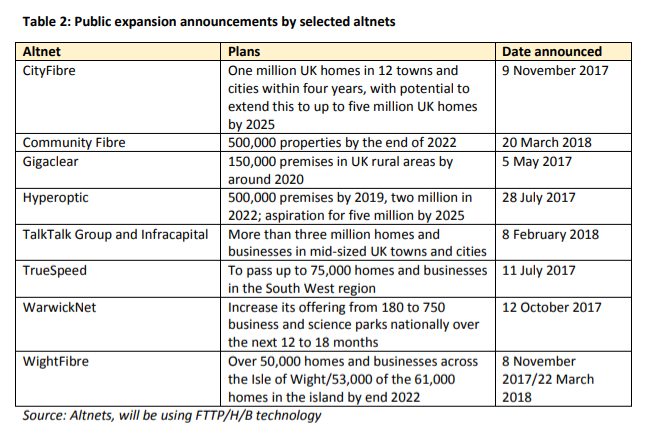

The notion of “premises addressed” is different. That term refers, according to a new report, as a location “located within x number of meters of a network.” That is different from the notion of a location “passed.”

Such “addressed” locations might be feasibly connected to the network, but are not actually “passed.” That concept likely grows from the competitive business services business, where the business model includes both “passed” locations and additional locations that can be profitably connected from existing facilities, but are not directly passed.

A new report by the Independent Networks Cooperative Association (INCA) and Point Topic suggests non-traditional service providers of “superfast internet access” (not telcos or cable TV operators) in the United Kingdom get about 21 percent take rates in areas where they can actively market their services.

“Superfast” is defined as downstream speeds of 30 Mbps or more.

The report does not count satellite, 4G, white space or leased line infrastructure accounts as part of the total subscriptions.

It is unclear whether the surveyed service providers are mostly the third or second provider of internet access services in their markets. A take rate of 20 percent would be notable even in a two-leading-supplier market (BT plus the “altnet”), but would be even more significant in a three-provider market (service is available from suppliers using the BT network--retail or wholesale--and Virgin Media and a third facilities-based supplier).

The point is that caution is called for, whenever new metrics are introduced.

No comments:

Post a Comment