Up to this point, in U.S. and Canadian fixed network markets, cable TV providers have had a capex advantage over telcos. Their hybrid fiber coax networks have proven less costly to upgrade to gigabit speeds than telco networks, which often must break with copper-based access to match such speeds.

So, up to this point, the telco business decision has been whether there is a clear payback from ripping out copper access and replacing it with fiber to the home. Although fixed wireless and advanced forms of digital subscriber line are solutions in niche cases, the big choice has been to make the transition to FTTH or not.

The range of choices will change in the 5G era, as fixed wireless becomes a potential "deploy at scale" choice in instances where the FTTH business case is difficult.

The “politically correct” answer to the question of whether 5G fixed wireless competes with fiber to the home access is that “both have their place,” or are complementary. That has been the PC answer to the question of whether FTTH competes with digital subscriber line or cable modems as well.

Always, the answers have to be contextualized. The cost of each particular solution, for particular deployments, must be weighed against expected financial return, especially in competitive markets dominated by facilities-based providers.

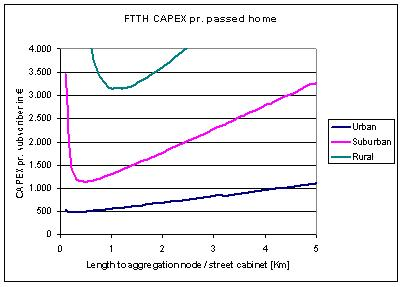

One key element is cost per passing. The other key variables include take rates and revenue per account. At a high level, fiber to the homes least (per passing) in urban areas, most in rural areas, and somewhere in between in suburban areas.

The cost of a fixed wireless solution likewise varies by density: lower costs per location when connecting a high-rise apartment building or condominium; higher costs to connect individual homes. But nearly all observers would likely argue that fixed wireless should be less expensive than fiber to the home.

Cost estimates arguably are most developed for use of fixed wireless frequencies long in use, more speculative for 5G-based millimeter wave bands, as volume production and use of small cell base stations is just beginning.

But cost per passing is only one of the key business model drivers. In competitive markets, where there are two or more equally-talented and capitalized providers, the addressable market is never 100 percent of locations. Instead, two strong competitors essentially will split the market.

And that means the cost per customer is roughly double the cost per passing.

In an era where one or multiple products might be sold, the average revenue per account also matters. And there, generally speaking, average revenue per account trends are clearly in the lower direction.

All of that--facilities-based competition; falling average revenue per account; cost per customer--means the cost of serving customers has to fall, even for next-generation networks that feature higher performance.

In that context, the question of “which platform” always includes a “cost to deploy” constraint. If the total customer base is limited because of competition, and average revenue per account is declining, then network cost (capex and opex) must drop.

That is why, all other things being equal, in competitive markets, the low-cost provider tends to win, when that provider has scale.

No comments:

Post a Comment