Sunday, July 23, 2017

Never Ring the Bell if You Want to Change the World

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Artificial Intelligence Could Boost Retail Sales 65% by Aligning Inventory with Demand

Artificial intelligence, internet of things, cloud computing, big data analytics and 5G are nearly impossible to clearly separate. All are parts of the expected emergence of “insight” as a major outcome and revenue driver.

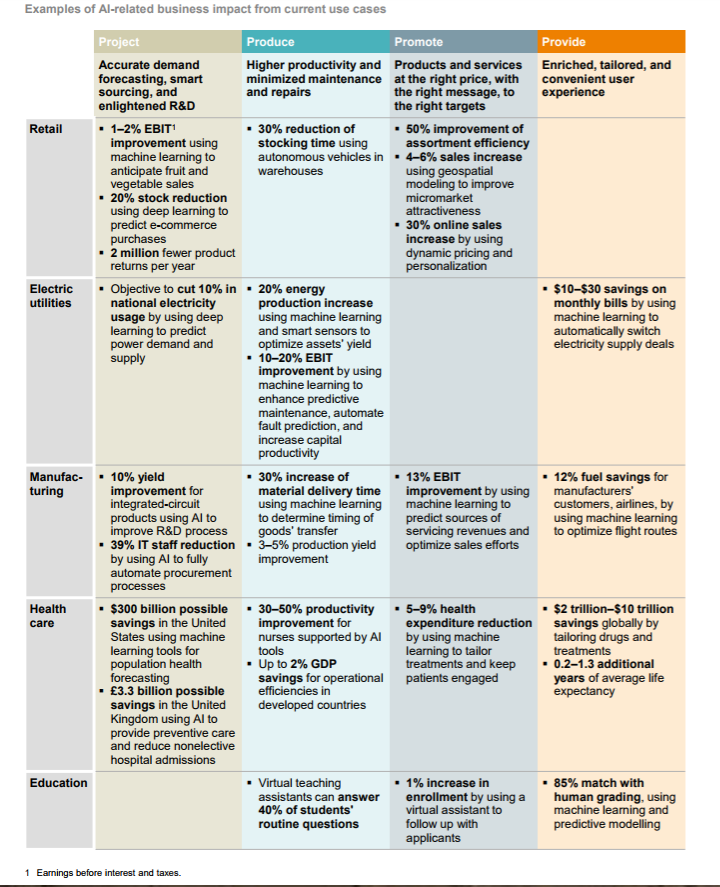

Better forecasts are one outcome. AI-based approaches to demand forecasting are expected to reduce forecasting errors by 30 to 50 percent from conventional approaches, according to McKinsey.

Lost sales due to product unavailability can be reduced by up to 65 percent when artificial intelligence is applied. Costs related to transportation are expected to decrease between five and 10 percent while warehousing and supply chain administration costs will decline 25 to 40 percent.

Using AI, overall inventory reductions of 20 to 50 percent are feasible, McKinsey estimates.

Most of that AI-enhanced processes are possible because of IoT.

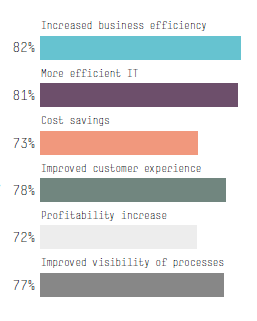

According to Aruba Research, 57 percent of companies have already adopted IoT and 85 percent are expected to do so by 2019. It is transforming the way companies do business and in a survey of global companies, the respondents' average return on investment was 34 percent with over a quarter of respondents reporting a 40 percent ROI and 10 percent of respondents reporting 60 percent ROI.

Some of the areas where IoT is having the biggest impact according to the percentage of respondents:

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

IoT-Assisted Parking Will See Winners and Losers

As with any other important economic change, internet of things will have winners and losers. Consider only the matter of parking costs. As that process becomes more efficient, consumers will pay less. But that also means sellers of parking spots and gasoline, to name a couple of examples, will earn less money.

Some retailers might incrementally gain store traffic, while online alternatives might incrementally lose a bit.

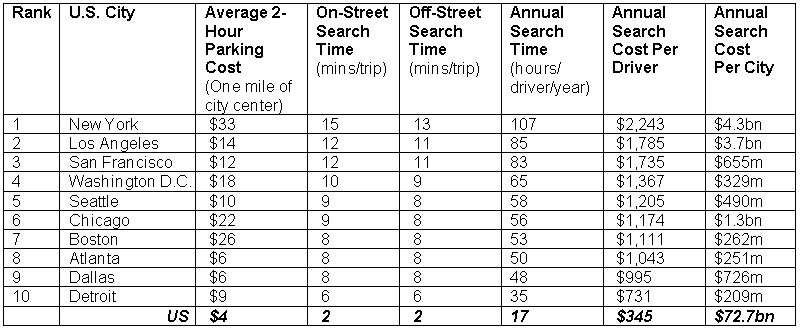

INRIX today published a major new study combining data from the INRIX Parking database of 100,000 locations across 8,700 cities in more than 100 countries, with results from a recent survey of nearly 18,000 drivers in the U.S., U.K. and Germany, including close to 6,000 across 10 U.S. cities.

On average, U.S. drivers spend 17 hours per year searching for parking at a cost of $345 per driver in wasted time, fuel and emissions, according to a study by Inrix.

On average, drivers in New York City spend 107 hours per year searching for a parking spot at a cost $2,243 per driver in wasted time, fuel and emissions, amounting to $4.3 billion in costs to the city as a whole.

Los Angeles drivers trailed New York with the most painful parking experience (85 hours – $1,785), followed by San Francisco (83 hours – $1,735), Washington D.C. (65 hours – $1,367), Seattle (58 hours – $1,205), Chicago (56 hours – $1,174), Boston (53 hours – $1,111), Atlanta (50 hours – $1,043), Dallas (48 hours – $995) and Detroit (35 hours – $731).

Hours Spent Searching for Parking

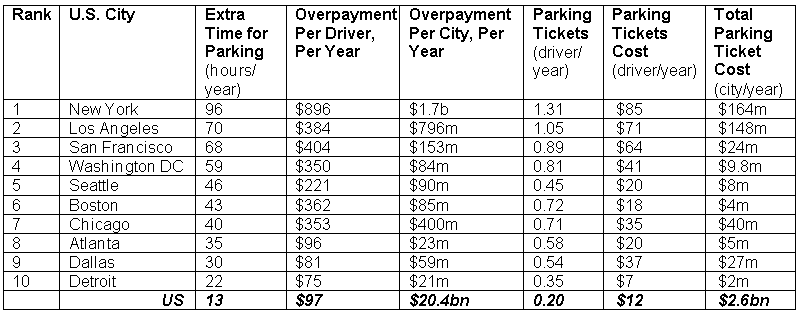

U.S. drivers also routinely pay for more parking, “just in case,” in the same way they buy mobile data plans larger than consumers expect to require, to avoid overage charges.

In the U.S., drivers add an average of 13 hours per year when they pay for parking. The cost of overpaying for parking amounts to more than $20 billion annually, on a national basis.

Drivers in New York City add the most extra time when paying for parking, averaging 96 hours a year, or an extra $896 in parking payments.

Extra Time for Parking Sessions and Parking Fines

Of the 6,000 U.S. drivers who responded to the survey, an alarming 63 percent reported they avoided driving to a destination due to the challenge of find parking.

Some 39 percent of respondents avoided shopping destinations because of the lack of parking, 27 percent didn’t drive to airports, 26 percent skipped leisure/sports activities and 21 percent avoided commuting to work. Some 20 percent of U.S. motorists surveyed did not drive to the doctor’s office or hospital due to parking issues.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, July 22, 2017

Shocking, Massive Changes Coming for Telecom

Not often is a slow-moving industry confronted by cataclysmic rates of change. But that is precisely what the telecom industry faces now. "Massive consolidation" and "spectacular change" are the ways Capgemini has characterized what is coming.

One example of the rate of change: Where today there are 800 telcos globally, by 2025 only about 105 will still exist, says Bell Labs. So within a decade, the industry will see the most-shocking consolidation in its history.

For most of its history, telecommunications was a monopoly, expensive and used by relatively few people. That meant one set of regulatory and policy issues, mostly centered on how to manage prices in a slow-moving utility industry.

All that changed in the late 1980s, when a global wave of privatization and competition began to take shape. For the first time, the policy framework shifted to ways to dismantle the monopoly regime and replace it with competitive markets.

- The business model is challenged, and could break

- Some countries might be forced back to “monopoly” facilities

- All the old revenue drivers will decline

- Massive industry consolidation is coming

- “Telecom” might not be the way the new industry develops

To prepare telecom professionals for all those changes, the PTC has created a new program called “Industry Transformation Boot Camp,” a week-long program explaining what is coming; why it is coming; what people plan to do about it; and why 5G will play such a prominent role in determining the outcome.

At the same time, as the wisdom of “everyone sells” has proven to be valuable, the next phase of industry transformation will require an “everyone thinks like a CEO” attitude, so fast, and so furious, will the changes be coming.

Created from two elements--Spectrum Futures (5G) and PTC Academy (“think like a CEO”), the boot camp will clearly explain what will happen (massive industry consolidation; business model collapse) and why. More importantly, boot camp attendees will learn why the changes are happening; what can be done to hasten the transformations and where the opportunities and dangers lie.

18–19 SEPTEMBER 2017

|

|

"THE INDUSTRY TRANSFORMATION BOOT CAMP"GROUP REGISTRATION AVAILABLEBEST VALUE | LEARN AND LEAD

Bring your team to Spectrum Futures 2017, book your registration, and save 20% per person when you register with a group of three or more.*

Taking place 18–19 September in Bangkok, Thailand, Spectrum Futures is gearing up for the “Industry Transformation Boot Camp," a new training program coordinated with the PTC Academy, PTC’s training event for Asia telecom professionals.

During the "Industry Transformation Boot Camp," invest in two days of in-depth discovery and the latest updates in mobile and 5G, completed by three days of PTC Academy, to master the intelligence and broader strategic context of the telecom industry.

Register now for the "Industry Transformation Boot Camp" – Spectrum Futures 2017 and PTC Academy, take advantage of exclusive group discounts available, and leap your career for success.

Email spectrumfutures@ptc.org to register your group, and we will assist you with all your attendance requirements.

*To qualify for group discounts, all delegates must be from the same company, and must register for the same registrant type and pay at the same time. Groups cannot retrospectively be compiled with delegates that have already registered.

|

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Industry Transformation Boot Camp: Register Now for Group Discount Rates

Bring your team to Spectrum Futures 2017, book your registration, and save 20% per person when you register with a group of three or more.

Bring your team to Spectrum Futures 2017, book your registration, and save 20% per person when you register with a group of three or more.

Taking place 18–19 September in Bangkok, Thailand, Spectrum Futures is gearing up for the “Industry Transformation Boot Camp," a new training program coordinated with the PTC Academy, PTC’s training event for Asia telecom professionals.

During the "Industry Transformation Boot Camp," invest in two days of in-depth discovery and the latest updates in mobile and 5G, completed by three days of PTC Academy, to master the intelligence and broader strategic context of the telecom industry.

Register now for the "Industry Transformation Boot Camp" – Spectrum Futures 2017 and PTC Academy, take advantage of exclusive group discounts available, and leap your career for success.

Get more details.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Overbuilder Business Model Still is Tough, Even When You Win

Perhaps few overbuilders have been as optimistic as Google Fiber about prospects for beating cable companies and telcos at the internet access game, but even Google seems to have found out how expensive and difficult the access game can be.

An important test is coming for overbuilder Ting in its south metro Denver markets, as it will face entrenched competition from both CenturyLink and Comcast, in an area where both those incumbents will be able to offer gigabit per second speeds to consumers.

Tucows, an overbuilder constructing gigabit internet access networks in a number of mid-sized towns, believes it eventually will reach 50 percent adoption rates (the adoption, or penetration rate, is the percent of homes in an area that are customers) in its markets after five years, a stunning figure that has been seen once or twice in U.S. overbuilder markets, but an achievement that remains quite rare.

At that level, an overbuilder would become the likely leader in its market.

Even expectations for the immediate future are healthy. “We expect to see 20 percent adoption among serviceable addresses in a year and 50 percent in five years,” says Elliot Noss, Tucows CEO. Generally speaking, an overbuilder with 20-percent share and control of its operating costs reasonably can expect to survive.

As was the case for overbuilders in the video entertainment business, and now with triple-play and internet access overbuilders, it has proven difficult to reach 20 percent market share after several years of operation.

As even the most-successful overbuilders have discovered, being the market leader is difficult, as the leader’s market share, in a competitive three-way market, might not exceed 30 percent or so of homes (potential accounts).

EPB in Chattanooga, Tenn., for example, is the poster child for overbuilder hopes, having gotten as much as 45 percent of consumer market share in its service area (with share defined as revenue-generating units, not “accounts” or “homes”).

EPB’s internet access share might be about 27 percent, its video share lower than that. An interesting statistic, in that regard, is that about eight percent of EPB’s internet access customers buy the gigabit service.

EPB’s market share is highly unusual in most overbuilder markets, as EPB arguably competes with Comcast, not AT&T, which has negligible video share in Chattanooga.

In a triple-play market, that is important. Comcast might have 61 percent video share, while EPB might have 36 percent share, leaving only three percent video share held by AT&T. Essentially, EPB has become the number-two provider, relegating AT&T to third place, something that is not the case in most other U.S. markets where three mass market fixed network suppliers compete.

AS well as EPB arguably has done, the overbuilder business model remains challenging. That is why fixed networks in many markets essentially remain monopolies at worst, despite deregulation, or at best oligopolies.

An important test is coming for overbuilder Ting in its south metro Denver markets, as it will face entrenched competition from both CenturyLink and Comcast, in an area where both those incumbents will be able to offer gigabit per second speeds to consumers.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Enterprise Customers More Satisfied than Small Business Customers (No Surprise)

Small businesses are significantly less satisfied with their telecom providers than large enterprise customers, the J.D. Power 2017 U.S. Business Wireline Satisfaction Study reports.

Small business customers face longer customer service wait times, lower problem resolution rates and less dedicated account support, all of which contribute to lower overall satisfaction with their telecom providers, J.D. Power says.

“Dedicated account support,” as many of you would guess, is part of the reason. Customers who have an account representative assigned to their business have notably higher levels of overall satisfaction (834) than those who contact a general call center (751).

Customers with a representative also have a more positive brand image of their provider and are more likely to characterize their telecom company as customer focused. Large enterprise customers are most likely to have an account representative (61 percent), of course.

The widest gaps in satisfaction between large enterprise businesses and very small businesses are in communication (804 vs. 701, respectively); cost of service (789 vs. 672); and customer service (818 vs. 695).

The average customer service hold time is 5.3 minutes for large enterprise customers; 5.9 minutes for small/midsize business customers; and 8.9 minutes for very small business customers.

“The small business telecom customer experience is very similar to the residential customer experience vs. large enterprise customers who are receiving a much higher level of dedicated service,” said Peter Cunningham, technology, media & telecommunications practice lead at J.D. Power.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...