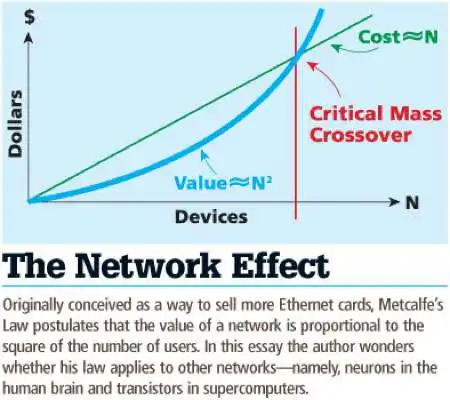

There is no inherent contradiction between any particular business model and obtaining scale or market share leadership, but there are imperatives to scale (network effects) in any ad-supported business model that might tell us something about the next wave of internet application development.

Put simply, will the next wave be driven by business models less dependent on network effects? If so, then the business need to drive scale by any means necessary (driving addictive or abusive behavior) will be less.

It remains impossible to pinpoint what the next period of app leadership will look like, except to say that observers expect a “next wave” to develop. The “post-Google, post-Facebook” era is hard to imagine, but subscription-based business models, with firms operating for long periods of time at lower volume (less scale) seem almost inevitable, given the building backlash against advertising-supported models.

Should privacy become a big-enough end user concern, then alternate revenue models based on subscriptions are nearly inevitable. Assuming one rules out donations as an attractive long-term model, there are few other options.

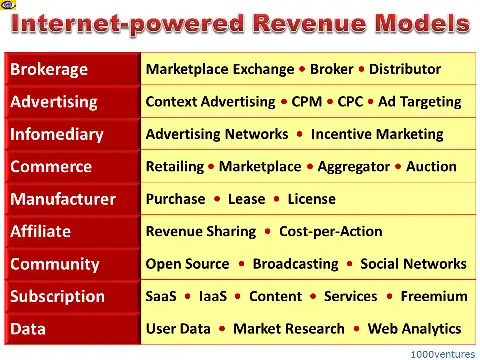

If one removes all revenue models dependent on monetizing user information, that mostly leaves subscriptions, commerce or device purchase (lease and rental being variants) as the main possibilities.

In principle, an appliance model (like purchasing a phone) is a conceivable, if far-fetched way to sell most applications. It is not without precedent, though. TiVo sold its time-shifted TV capability using both a subscription and device purchase model.

To the extent one conceives of in-home Wi-Fi as an application, there is a “rent or buy modem” model. In the business customer segment, there are subscription plans for Boingo venue Wi-Fi, if no device purchase model.

Still, in principle, a few highly-valued apps conceivably could be bundled with a device purchase. Think of a smartphone purchase that includes a two-year or three-year subscription to Netflix. It is a stretch, but is possible, if not terribly likely.

So if advertising models and device purchase models and donations are mostly infeasible, what remains? Mostly versions of the subscription model, or pay-per-use models.

And Facebook already has hinted that if the ad model is compromised, a subscription-based model that does not require intrusive profiling and behavior tracking could be created. That has important implications related to scale.

Most ad-supported consumer revenue models work best at scale, since most advertisers are used to buying on a “cost per thousand” basis. So the more “eyeballs” a venue commands, the more revenue it can earn.

Subscription models also are scale-dependent, up to a point, since but any single consumer is willing to spend relatively limited amounts of money on subscriptions. That obviously means there is a minimum number of “units sold” required to support firm operations.

The main point is that subscription models do not have the same “cost per thousand” business dynamics. Scale might be desired, but is not required, to the same extent.

Pay-per-use models also are conceivable, if logistically cumbersome. We are familiar with pay-per-use video or music models (buying songs or renting movies and shows). The cost of billing instances of usage that individually have small costs is one issue, but conceptually, micro-payments are possible.

The point is that, in the next era, if advertising does not drive revenue models, then something else will. Those other models arguably are less dependent on scale (cost per thousand) than advertising.

To be sure, there are many possible ways to implement a revenue model based on commerce, for example, though the challenge of creating an app model using commerce means the supplier has to avoid the “intrusiveness” and privacy issues that make “targeting” so useful for merchants.

And if opposition to retail data mining becomes vigorous enough, even the commerce model might not be so workable.

And that leaves one with subscriptions as the easiest alternative model.

Possibly significantly, that could mean a new era that initially begins again with lots of smaller providers. When consumers must buy apps on a subscription basis, they generally are picky about what they buy. So scale (volume) will be an issue for most app suppliers.

And that, in turn, answers the concerns about “bigness” and “lack of innovation” in the present era. If the advertising business model becomes toxic, subscriptions will be the main alternative for most potential apps. And that will mean, at least for a time, that bigness is not so much an issue, as demand will be fragmented.

The point is that markets tend to work, when customers are able to make choices with low friction. A big shift away from ad-supported apps is going to mean some present problems (privacy, perceived barriers to innovation) will tend to fix themselves.

There is no easy way to solve the problem of bad manners, aggressive behavior and courtesy, though. But peer pressure seems to work well enough, in other areas of life. What we now need, to fix the “bad manners” problem, is enough peer pressure from people to shame abusers into exhibiting good manners.